• Manufacturing industry output will start to recover in 2025, albeit slowly

• 2024 has been particularly difficult for traditional market sectors

• Strong growth in semiconductors in 2024, but destocking in industrial automation

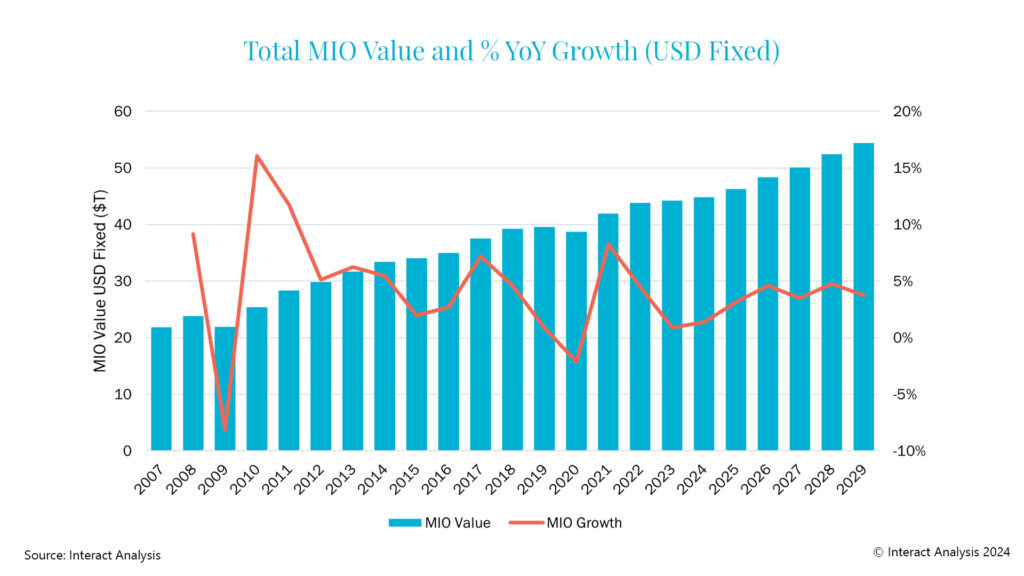

The manufacturing industry will experience a recovery in 2025, but the latest forecast from Interact Analysis has softened for most regions, as the slowdown appears ‘stickier’ than expected and could bleed into next year. This has resulted in a weaker than previously predicted recovery in 2025, but manufacturing is expected to return to normal by 2026 and the market intelligence specialist does not foresee any major problems for the sector by the end of the decade.

According to the latest Interact Analysis Manufacturing Industry Output (MIO) Tracker, 2024 has proved particularly tough for many industries, including traditional market sectors such as commercial vehicles, pulp & paper, textile and those linked to construction.

Semiconductor production to make a strong recovery in 2024

An anticipated strong recovery in the semiconductor sector during 2024 will benefit APAC economies such as South Korea, Singapore and Taiwan, which struggled in 2023 from low demand in a major industry.

In other sectors, many machinery OEMs are outperforming their industrial automation component suppliers as demand for both has weakened. The industry appears to be going through a period of destocking, there is hesitancy among its customers to invest in upgrading machinery while interest rates remain high, and many of the sectors that require machines that use drives, motors and geared motors are currently in a slump.

Manufacturing output growth for 2025 has been revised as the downturn continues to bite

Europe and the Americas bearing the brunt of the downturn

The regions primarily affected by the downturn are Europe, and to a slightly lesser extent the Americas; with stronger indicators within some major regions of APAC continuing to grow, albeit more slowly than in recent years.

In Europe, automotive has the strongest CAGR of any sector at 4.6% over the next 5 years, despite its recent struggles, while APAC is performing best in the semiconductor & components industry; and transportation sectors are growing in the Americas due to infrastructure investment across the region.

Commenting on the latest MIO Tracker, Interact Analysis Senior Data Analyst Jack Loughney says, “The machinery sector is in a difficult spot. Machinery demand is much more volatile than general manufacturing demand and every downturn has seen machinery performing worse than the general economy. As manufacturing sectors leave their own downturns, we expect machinery to return strongly in most cases with equipment such as packaging and semiconductor machinery expected to perform well.”