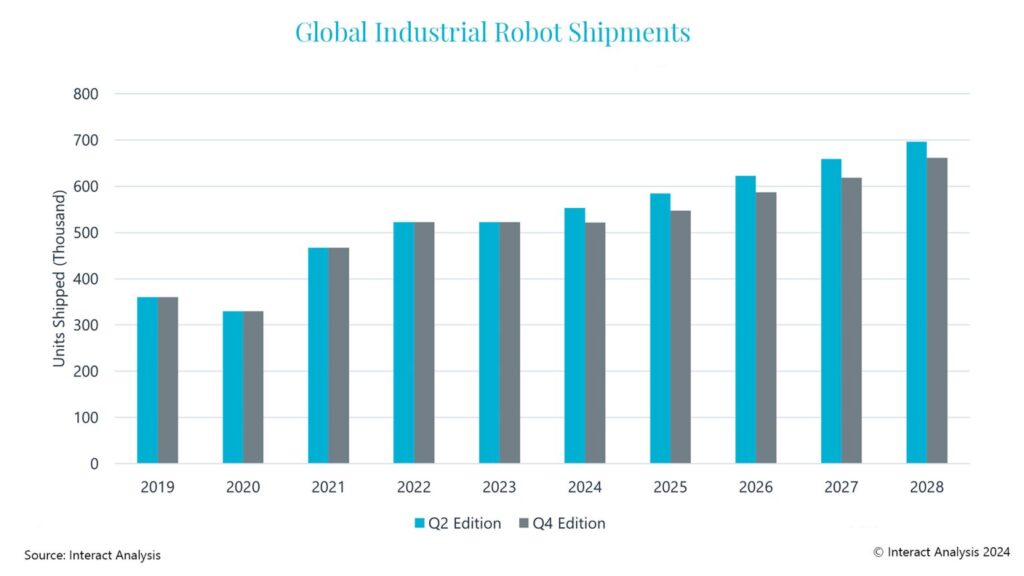

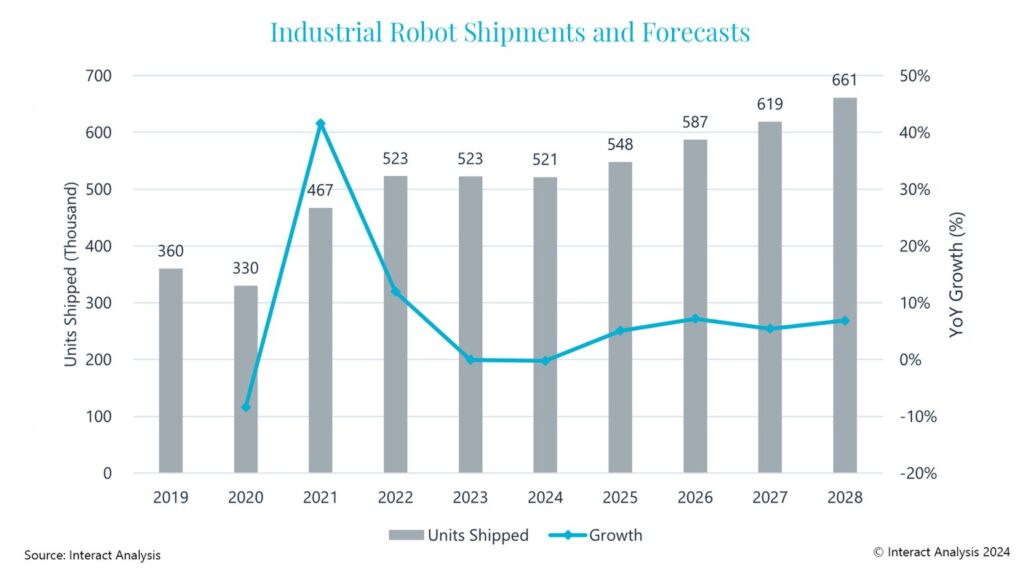

The industrial robot market is facing a mixed picture over the coming years, with 2024 set to end on a challenging note. Global robot shipments are projected to decline by 0.2%, following a flat performance in 2023. Compared with our May 2024 forecast, we have revised our 2024 projections for overall shipments downward by 5.8%; from over 553,000 units to 521,328 units. Additionally, the expected growth for 2025 has been reduced by 0.7 percentage points. These revisions reflect weaker-than-anticipated sales to the automotive industry in the second half of 2024 within the US and Europe, along with continued sluggish demand in China.

Our forecast for robot shipments in 2024 and beyond has been revised downward.

Despite these challenges, we expect a gradual recovery in 2025. This is driven by anticipated increases in machinery investments – as key economies lower interest rates – alongside a broader recovery in the global manufacturing sector. However, factors such as high inventory levels and weak order intake are likely to persist in many industry sectors. This could potentially dampen robot demand during the first half of 2025. We forecast that industrial robot shipments will return to growth rates of over 7% by 2026.

We expect global robot shipments to reach 548,000 units in 2025

Market by Robot Type:

Collaborative robots (cobots) stand out as a key growth area. We expect to see a 15.9% increase in shipments in 2024, despite the global economic slowdown. However, as competition increases, the price decline for cobots has been the most pronounced, resulting in a slower projected revenue growth rate of 11% during 2024.

SCARA robots are expected to see modest growth of 1.8% in 2024, fuelled by demand recovering in Asia’s semiconductor and electronics sectors. In contrast, other robot types will experience declines in shipments of 1-3% over the year, primarily due to challenges within the automotive and broader industrial sectors.

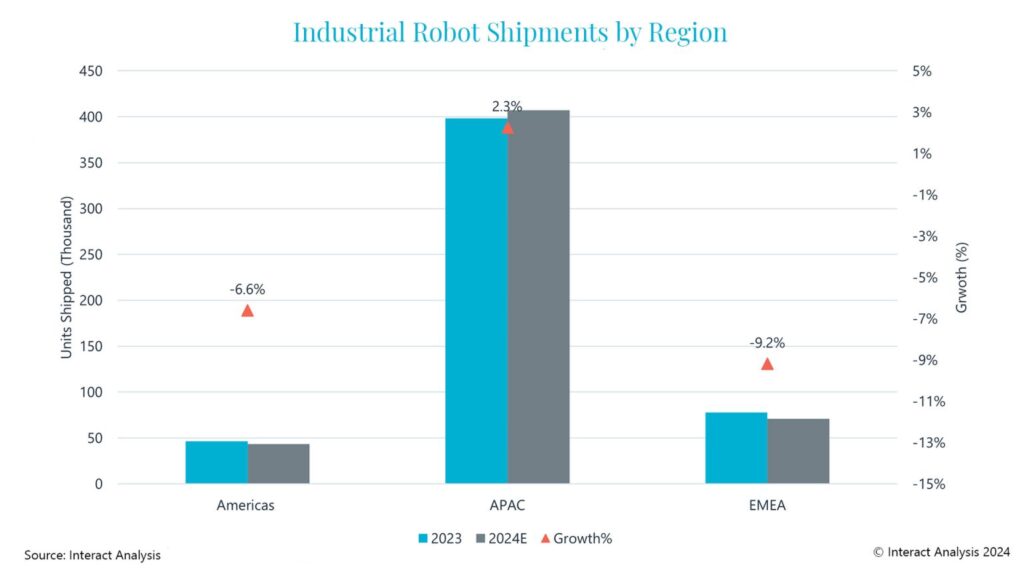

Regional Market Dynamics:

Americas:

Robot shipments in the Americas are projected to contract by 6.6% in 2024, primarily due to sluggish demand from the automotive industry. Shipments in the electronics and metal sectors are also experiencing declines. While demand for robots in consumer-related sectors is growing, it is not enough to offset the downturn in other industries. However, the life sciences sector has been a bright spot, with strong growth in demand for robots used in pharmaceutical production and medical device assembly in the US.

From 2024 to 2028, industrial robot shipments in the Americas are expected to grow at a CAGR of 6.1%. After the double-digit growth seen in 2021 and 2022, it is expected that the market will stabilize and expand at a more moderate pace in the coming years. We anticipate the continued trend towards greater automation and US reshoring initiatives will support the growth of manufacturing and demand for robots in the region.

Asia Pacific:

In 2024, robot shipments in Asia Pacific are expected to increase by 2.3%, driven by a 3.3% increase in China and a 4.9% rise in the rest of APAC (excluding Japan and South Korea).

- The Indian manufacturing industry continues to experience strong growth in 2024, spurred on by government investments in infrastructure. Industrial robots are rapidly gaining traction in India.

- The robot market in Taiwan and Southeast Asia is also seeing steady growth, fuelled by recovery of the semiconductor industry.

- China’s manufacturing sector is facing another challenging year in 2024. Due to overcapacity in the EV battery and solar panel industries, robot shipments in these sectors are expected to decrease by nearly 10%. Additionally, robot demand in the automotive and electronics sectors is expected to show only modest growth.

From 2024 to 2028, robot shipments in Asia Pacific are projected to grow at a compound annual growth rate (CAGR) of 6.2%. Excluding China, South Korea and Japan, the region is expected to record a CAGR of 7.4%. Southeast Asian countries are emerging as key hubs for the electronics, semiconductor, and automotive industries, with international companies increasingly establishing factories there. This is expected to help drive robot demand.

Europe, Middle East and Africa (EMEA):

In 2024, robot shipments in EMEA are expected to decline by 9.2%. In Europe, orders sharply deteriorated in the second quarter, particularly in the automotive sector. Like North America, robot shipments in the European life sciences and food & beverage industries are expected to see smaller declines (2-3%), in contrast to the larger contractions anticipated in industries such as automotive, metal, and rubber & plastics. Although the new energy segment in Europe is comparatively small, it is also expected to experience a significant drop in robot shipments.

From 2024 to 2028, we expect robot shipments in the EMEA region to grow at a CAGR of 5.6%. Demand growth in Eastern Europe is expected to accelerate with the expansion of the automotive supply chain in the region. Specialist countries in the life sciences sector, such as Denmark and Switzerland, are also expected to see above-average growth. However, larger manufacturing hubs, like Germany, are anticipated to experience slower growth, due to the ongoing recession in the manufacturing sector and structural challenges that could hinder economic recovery.

Americas and EMEA are expected to see declines in robot shipments during 2024.

Final Thoughts

In conclusion, the industrial robot market is navigating through a period of instability, with regional and sector-specific challenges influencing overall growth. While 2024 is a year of contraction, the medium-term outlook is more positive, especially as economic recovery gains momentum and new opportunities arise for automation.