Sales up 5% over 2024 but Order Book flat – Interconnect Technologies Suppliers Association (ITSA)

Headline performances: –

- Revenues up 5% yoy and orders flat yoy

- B to B flat 1:1.

- Key Markets: –

- Broadcast down 6%.

- Mil/Aero up 2%

- Medical up 12%

- T&M down 13%

- Mass Transport up 57% (This is linked to key rolling stock and infrastructure projects)

- Smaller Markets: –

- Automotive up 22%

- Comms down 7%

- Data down 4%

- Distribution continued to perform well with an increase of 12% yoy.

- Technology Shifts

- Fiber Optics up 5%

- RF down 16%

- Circular up 17%

- Value Add up 41%.

Overview.

2025, what a year of challenges. Tariffs, Tantrums and Threats. Budgets and policies with so many U turns you would be forgiven for thinking they were created by a driving school. The conflict in Ukraine which shows no immediate sign of coming to a ceasefire, unrest and instability around the middle east and Europe realising that it must look after itself, but, despite all of this the stock markets remained buoyant, the UK connector market grew again and ITSA members enjoyed a reasonably positive year.

Interconnect revenues grew 5% in 2025 which was very much in line with our members projections and investments continued, however, employment has been drastically affected by the uncertainty over any new employee legislation and the increase in the minimum wage, as previously reported members continue to look at innovative in house employee development rather than external recruitment .

Orders did not grow in 2025, so we enter 2026 with a slightly decreased order backlog.

A positive sign is that members distribution revenues were up 12% which has historically led to increased OEM revenues and our key strategic markets were all positive.

At a technology level all key interconnect products were up with the exception of RF, however, this has to be offset by the increase of 41% in members value add activity which indicates a focus on things such as cable assemblies and sub systems which incorporate a lot of RF interconnect.

For 2026 members are looking at low single digit growth again but this could be higher as there are a lot of key programmes in the pipeline for 2026 and beyond.

As with previous years the UK interconnect market has proved to be challenging but amazingly resilient.

Members are planning for a face-to-face meeting in May where we will conduct a comprehensive review of the associations activities and to agree forward plans regarding PR, Web enhancement, social media engagement, membership, and market trends.

External UK Economy reports used.

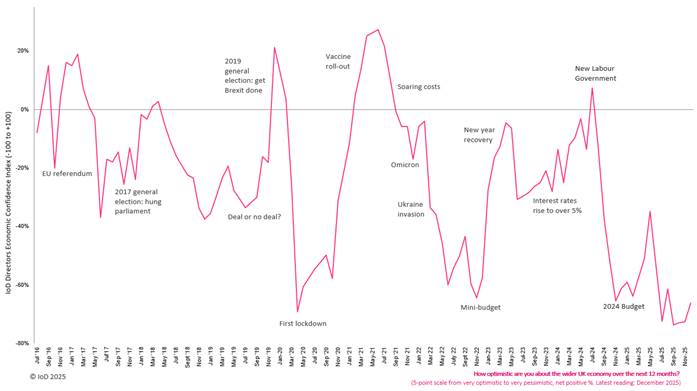

- The IoD Directors’ Economic Confidence Index, which measures business leader optimism in prospects for the UK economy, ticked up to -66 in December 2025 from the (pre-Budget) November level of -73.

- Once business leaders had a little more time to reflect on the impact of last year’s Budget on confidence in their own organisations, it was little changed in December 2025, at -4, from -5 in November.

- Most underlying economic measures were either stable or worsened in December compared with directly before the November Budget – with the exception of those for costs:

- Headcount expectations dropped to -14 in December from -8 in November

- Investment intentions dropped to -21 from -17

- Cost expectations fell marginally to +84 from +86

- Export expectations were little changed at +5 from +6

- Revenue expectations were little changed at +8 from +7

- S&P Global UK Manufacturing.

UK manufacturing recovery continues at end of 2025 as output and new orders edge higher December 2025 Manufacturing PMI at 50.6 in December (15-month high) Production growth supported by stock building and new order uptick Input price inflation accelerates December saw further signs of growth emanating from the UK manufacturing sector. Output rose for the third successive month and new orders increased for the first time since September 2024. There were also signs of the trends in new export orders and employment moving closer to stabilising after sustained downturns.

The seasonally adjusted S&P Global UK Manufacturing Purchasing Managers’ Index™ (PMI®) rose to 50.6 in December, from 50.2 in November, its highest level for 15 months but below the earlier flash estimate of 51.2. The PMI has posted above its neutral 50.0 mark (separating growth from decline) in each of the past two months.

Three of the PMI sub-components registered readings consistent with improved operating conditions in December, as output and new orders both rose, and suppliers’ delivery times lengthened. Although stocks of purchases and employment both declined, this was to lesser extents than in November. The latest increase in manufacturing production reflected a building-up of stocks of finished products and efforts to clear backlogs of work. UK manufacturers also benefited from several reduced headwinds towards the end of the year, as the negative impacts of uncertainty surrounding the Autumn Budget, tariffs, and the JLR cyber-attack all moderated. Output rose across the consumer, intermediate and investment goods sectors, the first-time concurrent growth has been registered since August 2024.

- Make UK report.

https://www.makeuk.org/docs/executive-survey-2026pdf/download?attachment