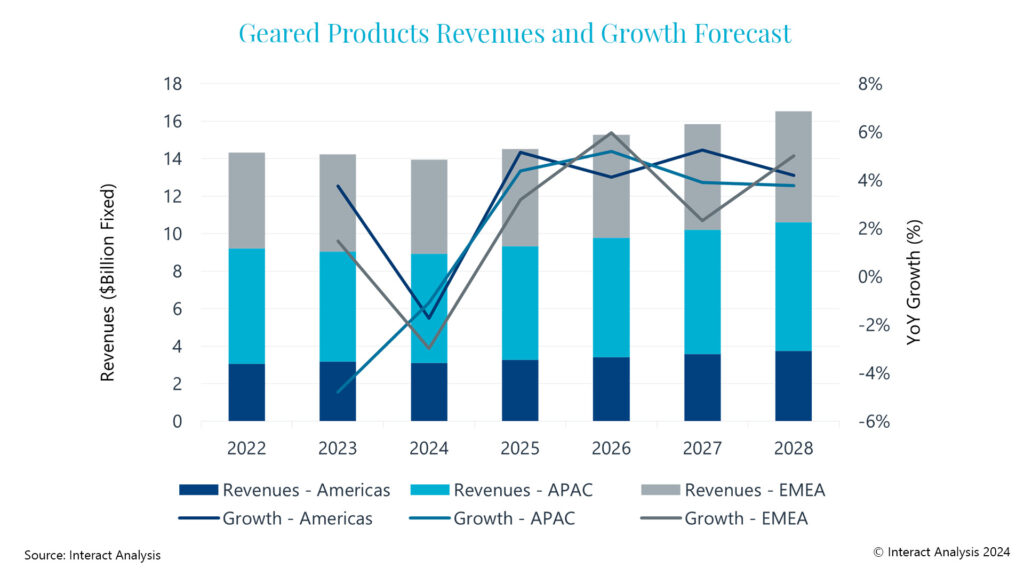

- The geared products market will grow by 3-5% per year between 2025 and 2028.

- Asia Pacific (APAC) is the largest market for geared products.

- The vendor landscape for the market continues to concentrate.

London, 4th January 2024 – The geared motors and industrial gears market experienced a decline in 2023 following strong growth in 2022. According to global market intelligence firm Interact Analysis, further market contraction is expected in 2024 before recovering in 2025.

Interact Analysis’ latest research found that many gearbox suppliers observed a slowdown in order intake in the second quarter of 2023, leading to an expected market revenue contraction of 0.7%. This dip is expected to continue into 2024, leading the firm to forecast a further revenue decline of -1.9% for the geared motors and industrial gears market next year. However, the outlook appears to be rosier for 2025 and beyond, with steady growth expected of ~3-5% per year out to 2028.

Despite a slow year for the market in 2023, the global geared products market was worth $12.6bn in 2022, representing year-on-year growth of 1.4%. Price increases played a significant role, as average selling prices of geared products rose by 5-10% in 2022 fueled by raw material costs, supply chain problems and rising energy prices.

A regional perspective

Taking a look at the market by region, APAC is by far the largest for geared products, representing 46% of global revenues. This is followed by EMEA and the Americas with shares of 33% and 21% respectively. Revenue growth in the Americas outpaced EMEA in 2022 as a result of strong demand and strong currency. The market in the Americas grew by 12% in 2022, compared with just 1.1% in EMEA and -2.7% in APAC.

APAC is the largest market for geared products followed by EMEA and the Americas.

However, in 2023, the APAC region is expected to have experienced the largest contraction, while the Americas region is forecast to maintain reasonable growth. This decline in APAC is largely due to the contraction that has been observed in China and the impact of the property slump on this market. It is expected that Indian and Southeast Asian markets will prop up revenue growth of geared products in APAC over the next couple of years.

Samantha Mou, Research Analyst at Interact Analysis, comments on the supplier landscape for the geared products market, stating, “The leading vendors for the geared products market remain relatively unchanged, but concentration of the supplier base continues. As a result of its acquisition of Altra Motion, Regal Rexnord is now among the top 5 leading global suppliers of geared products.

“Overall, the ranking of other leading vendors remains stable, with SEW Eurodrive retaining its position as the #1 vendor globally and across all tri-regions. The EMEA vendor landscape is the most ‘stable’, with all leading suppliers enjoying growth in their specialized areas in 2022.”

About the Report:

This report is the 4th edition of our Geared Motors & Industrial (Heavy-duty) Gears Market report.

We have conducted extensive interviews with leading vendors in the industry to capture market performance, trends and development, etc. to ensure the quality and accuracy of our work. Coupled with our “tertiary-level” dataset, users of the report are able to view market sizes and forecasts by geared product type, by torque, by industry, and by country.